3 Questions I Ask Before Every Small Cap Investment

I invest in small caps two ways — GARP and deep value. Here are the 3 questions I use to separate real opportunities from value traps, with real case studies.

Nearly every stock has a price where it's an attractive buy. The challenge is finding the ones where that price is today's price.

In small cap investing, these opportunities show up more often than most people realize. Higher volatility, thinner analyst coverage, less institutional participation, structural forced selling from spin-offs and index rebalancing, minimum market cap and price thresholds that lock out large funds — all of it creates mispricings that simply don't exist in large caps. A $50 billion fund can't take a meaningful position in a $200 million company. That structural gap is where I spend most of my time.

I look at over 200 ideas per week through Pelican's screening pipeline. Before any of them get serious research time, they have to pass three questions. But the way I apply those questions depends on what kind of opportunity I'm looking at. I invest in two distinct buckets — GARP and deep value — and while the three questions are the same, the answers look very different.

The Two Buckets

GARP (Growth at a Reasonable Price) is where I look for high-quality businesses trading at reasonable multiples. These are companies with high ROIC, durable competitive moats, and secular tailwinds — but something temporary has compressed the valuation. The bet is that the market is overweighting a short-term problem and underweighting the long-term earning power.

Deep value is where I look for stocks trading below what the assets are worth today. Low price-to-tangible-book, heavy insider ownership, commodity-tied cyclical businesses where the market is pricing in permanently depressed conditions. The bet here isn't on growth — it's on reversion to the mean and the margin of safety embedded in hard assets.

Both strategies share the same core belief: the market misprices small caps more frequently and more severely than large caps. But the toolkit for each is different. Let me walk through both.

Question 1: Is the Valuation Actually Attractive?

This is the entry point for everything I do. If the price isn't compelling relative to what I'm buying, nothing else matters.

For GARP, I'm looking for quality businesses trading under 20x EBITDA with strong returns on invested capital. High ROIC is a proxy for business quality — it tells you the company is generating real economic value, not just revenue. I want to see historical revenue growth, secular tailwinds in the industry, and a competitive moat — network effects, switching costs, scale advantages — that protects margins over time.

For deep value, the bar is different. I want to see a price-to-tangible-book near or below 1x, the stock trading below peer multiples, and ideally hard assets that the market is undervaluing — long-owned real estate, idle plants, fleet assets, or inventory that could be liquidated for more than the market cap implies.

In both cases, I'm also looking for high insider ownership. I want management teams whose net worth rises and falls with the stock price — not hired-gun CEOs collecting a salary regardless of performance. Aligned incentives change how capital gets allocated.

What kills an idea at Question 1

Secular decline. A cheap stock in a structurally shrinking business is almost never a good investment, regardless of the multiple. Take BTMD — a hormone optimization platform trading at roughly 2x earnings with Q4 2025 procedure revenue declining 13% as clinic attrition accelerates. The P/E screams "cheap," but the core business is contracting. No amount of valuation discount compensates for a melting ice cube.

Question 2: Why Does This Opportunity Exist?

If a stock looks cheap, there's a reason. You need to understand that reason before you can determine whether it's a real opportunity or a trap.

I'm looking for a legible reason for mispricing — something specific and identifiable that explains the discount, and that I believe the market has wrong. The best small cap opportunities come from a handful of recurring patterns:

- Neglect. No analyst coverage, too small for institutional mandates, recently spun off with no natural shareholder base. The stock isn't mispriced because someone analyzed it and disagreed — it's mispriced because nobody's looked.

- Temporary operational drag. A bad quarter, a money-losing division, a one-time charge that the market extrapolates as permanent.

- Cyclical trough. A commodity-tied business at the bottom of its cycle, where the market is pricing in permanently depressed margins.

- Sector contagion. The entire sector sold off on a macro headline, and the strongest operators got unfairly punished.

- Complexity. A restructuring, divestiture, or management transition that makes the financials messy and hard to model. Most analysts give up. The few who do the work find the value.

If I can't articulate a specific, falsifiable reason why the market is wrong, I don't have a thesis — I just have a cheap stock.

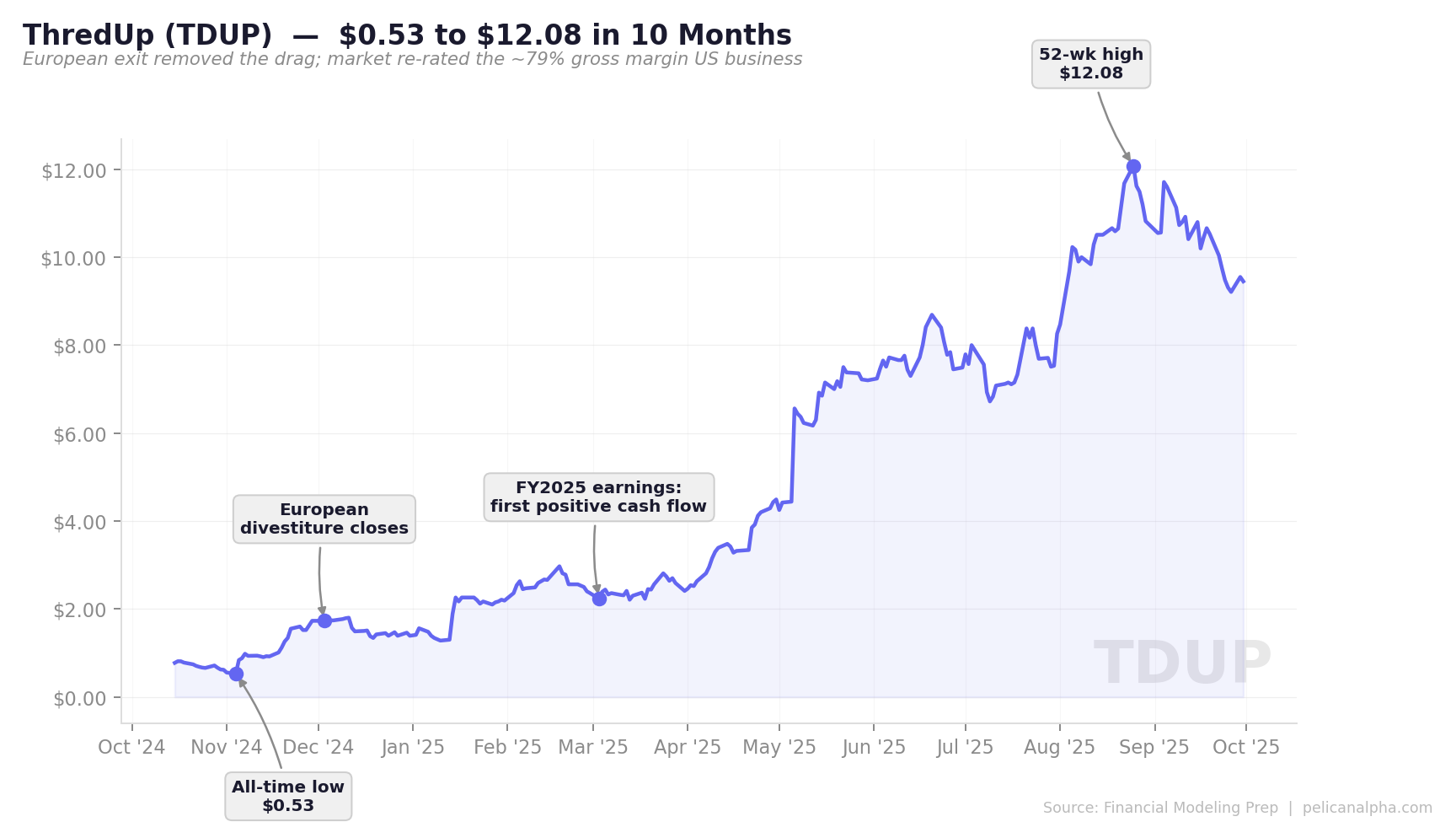

GARP Example: ThredUp (TDUP)

TDUP | Online Resale / Consumer Marketplace | Temporary operational drag

ThredUp is one of the largest online resale platforms in the US and the largest managed resale marketplace — sellers ship in clothing and ThredUp handles pricing, photography, listing, and fulfillment. The US-only business runs at ~79% gross margins with 20% revenue growth and strong secular tailwinds (the global secondhand apparel market is projected to reach $486B by 2031 per Research and Markets, growing at ~16% annually).

So why was the stock trading at $0.53 in November 2024 — down 98% from its IPO high?

The answer was Remix, a European resale platform ThredUp acquired for $28.5M in 2021. Remix ran at 24% gross margins versus 80% in the US and was bleeding cash at a negative 23% adjusted EBITDA margin. The European division was masking the quality of the core business. Every consolidated financial statement made ThredUp look like a money-losing operation with no path to profitability.

The mispricing was legible: the market was valuing the whole company based on blended metrics that included a division destroying value. Strip out Europe, and you had a high-margin marketplace with network effects, 163 brand partners on its Resale-as-a-Service platform, and a durable competitive moat built on $400M+ in proprietary reverse logistics infrastructure.

Before exit (Nov 2024) → After exit (2025):

- Stock price: $0.53 (all-time low, Nov 4) → $12.08 (52-week high, Aug 25)

- Gross margin (US): 80% (masked by Europe's 24%) → 79.4% (reported clean)

- Adj. EBITDA margin: Negative (blended) → 4.4% and expanding

- Active buyers: Declining → 1.65M (+30% YoY, record)

- Annual cash flow: Negative → +$3.1M (first-ever positive)

ThredUp announced the European exit in August 2024 and completed the divestiture in early December. The stock bottomed at $0.53 on November 4, started 2025 at $1.41, and ran to $12.08 by late August 2025 — roughly 23x from the absolute low and 8.5x from the start of 2025. First positive cash flow year in company history. The business didn't change. The market's ability to see it clearly did.

Question 3: What Re-Rates This Stock?

A stock can be cheap for years. A business can be improving for years. Neither fact alone puts money in your pocket. Something has to change the market's perception — and ideally, I can identify what that something is before it happens.

This is the catalyst question, and it's where I separate ideas I watch from ideas I put capital behind.

Good catalysts are specific and time-bound:

- Earnings inflection. Consensus estimates haven't caught up to improving fundamentals. This is the most common catalyst in small caps because analyst coverage is thin and estimate revisions lag.

- Insider buying clusters. Management and board members buying stock with their own money — not exercising options, writing checks. As I covered in How to Read 13F Filings, following smart money works when you understand the context. Insider buying in a small cap with improving fundamentals is one of the strongest confirming signals I know.

- Activist involvement. An activist investor taking a position and pressuring for change — asset sales, board seats, strategic review. When I was at Osmium Partners, we ran these campaigns ourselves. As a passive investor now, I look for situations where someone else is creating the catalyst.

- Capital return. Buybacks or dividend initiation signal management confidence and attract new investors.

- Strategic activity. M&A in the sector, a competitor getting taken private, or comparable transactions that highlight the valuation gap.

The key word is specific. "The market will eventually realize this is cheap" is not a catalyst. "Crush margins just hit $0.91/gallon — up 435% from last year — and Q3 earnings will reflect it before the street updates estimates" — that's a catalyst with a date and a mechanism.

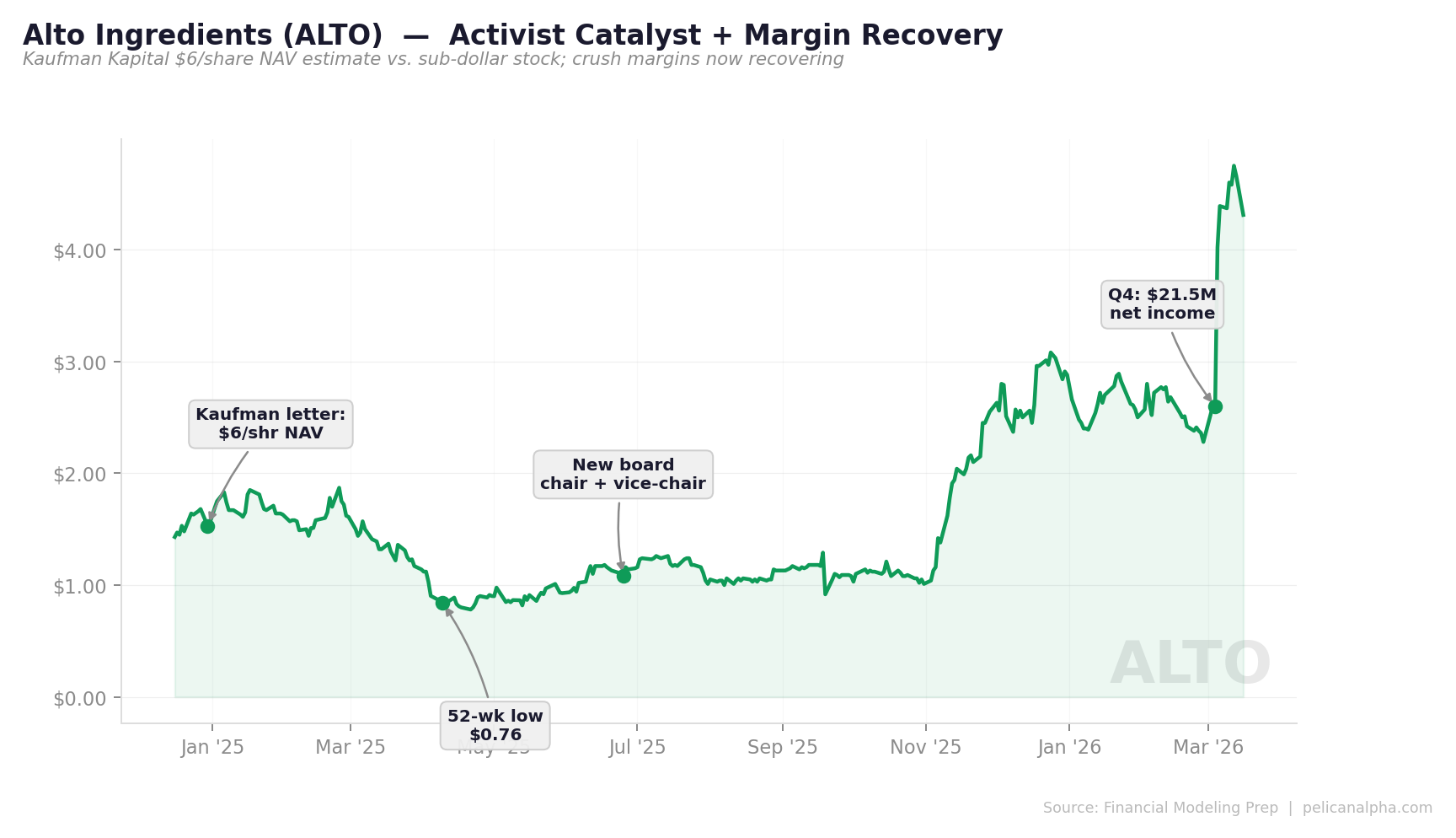

Deep Value Example: Alto Ingredients (ALTO)

ALTO | Ethanol / Renewable Fuels | Cyclical trough + activist catalyst

ALTO is an ethanol producer — a commodity-tied, cyclical business with ~350 million gallons of annual production capacity across five plants. This isn't a new pattern for ALTO — in the COVID crash of 2020, the stock traded down to a $14M market cap before rallying over 3,500% as crush margins recovered. The market has a habit of pricing ethanol producers for death during cyclical troughs, then scrambling to reprice them when margins revert.

By late 2024, crush margins had compressed again and ALTO was trading near $1.68 — well below tangible book value. Activist investor Kaufman Kapital (~4.9% ownership, the largest stockholder) published a letter in December 2024 estimating ALTO's plants were collectively worth $550M+ (~$6/share) and pressured the board to explore strategic alternatives. For context, when GEVO announced the acquisition of Red Trail Energy's 65M gallon ethanol plant in September 2024 for $210M (including carbon capture assets, deal closed February 2025), the implied valuation was $3.23/gallon of capacity. Even discounting for the CCS premium, that comp implies ALTO's capacity is worth multiples of its market cap.

Late 2024 (Kaufman letter) → March 2026:

- Stock price: ~$1.68 → ~$4.30

- Kaufman NAV estimate: $6/share (still implies upside)

- Price vs. Kaufman NAV: ~0.28x of estimated asset value → ~0.72x

- Q4 net income: -$42.0M (Q4 2024) → +$21.5M (Q4 2025)

- Crush margins: Compressed → Recovering

What was the catalyst? Activist pressure + earnings inflection. Board changes followed Kaufman's letter — new chair and vice-chair installed in June 2025. Then crush margins started recovering, and Q4 2025 delivered $21.5M in net income versus a $42M loss in the prior year's quarter. The stock bottomed at $0.76 in April 2025 and has since rallied to $4.30 — a 5.7x move in under a year, with the activist's $6/share NAV estimate still implying meaningful upside.

This is what deep value looks like in practice: hard assets trading at a fraction of replacement cost, an activist creating urgency, and a cyclical turn delivering the earnings catalyst the market needed to re-rate.

Deep Value Requires More Nuance

I want to be honest about this: deep value is harder than GARP. There are more ways to lose money. The checklist is longer and the margin for error is thinner.

Beyond the three questions, here's what I stress-test in every deep value situation:

- Zero solvency risk. I sensitize commodity prices to worst-case scenarios. What would it take for this company to go bankrupt? If the answer involves even moderately adverse conditions — negative free cash flow, heavy debt maturities, rising interest rates — I pass. The whole thesis depends on surviving to see the reversion.

- Not in secular decline. This is the single most important filter. Cheap cyclical businesses can recover. Cheap businesses in structural decline usually don't. I need to believe the industry has a future, not just a past.

- Hidden or undervalued assets. Long-owned real estate carried at historical cost, fleet assets worth more as scrap than the market cap implies, idle capacity that has option value if conditions improve.

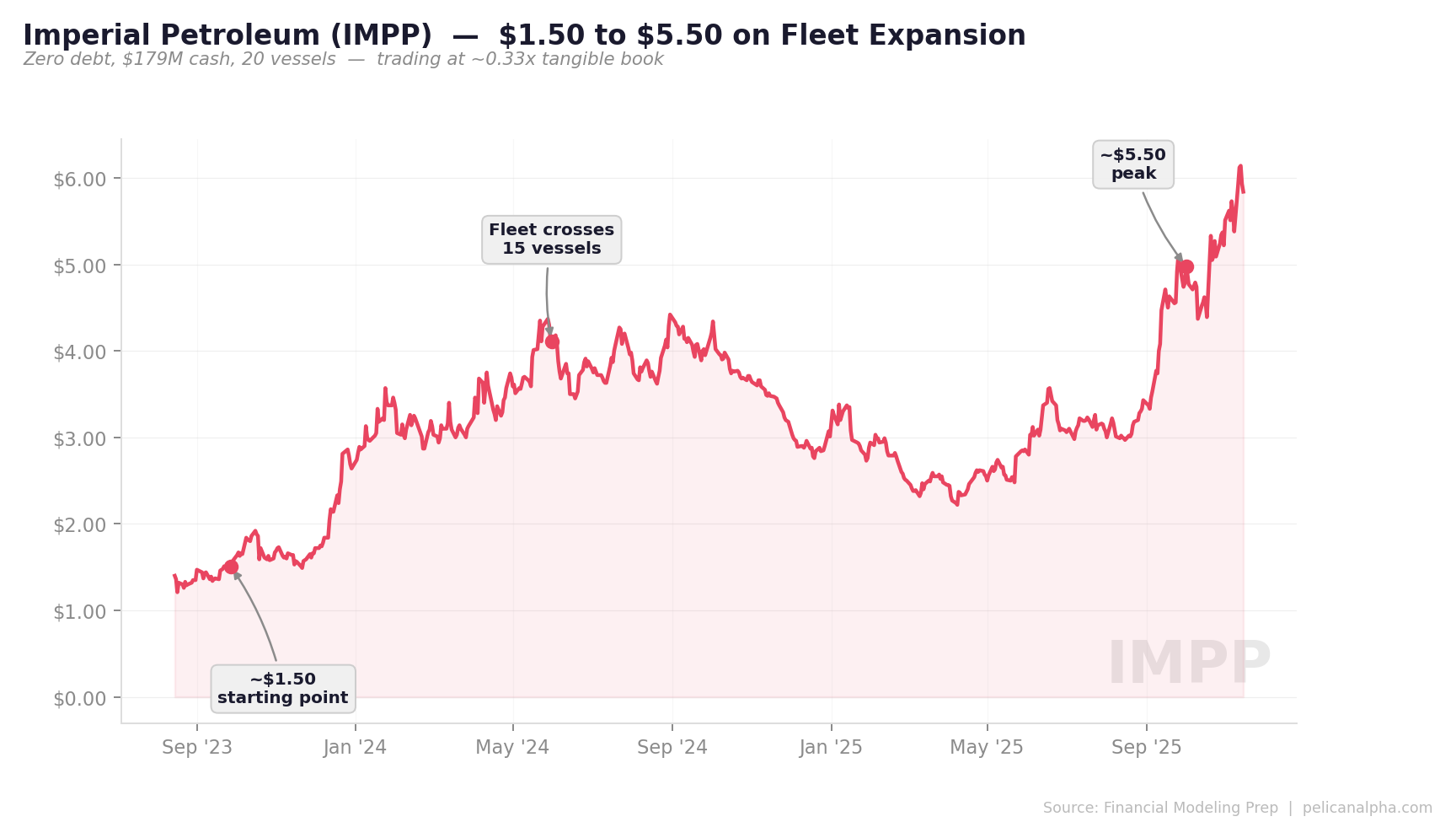

Deep Value Example: Imperial Petroleum (IMPP)

IMPP | Shipping (Tankers + Drybulk) | Asset discount + governance overhang

IMPP is a Marshall Islands-incorporated shipping company headquartered in Athens that illustrates both the opportunity and the complexity of deep value. Here are the numbers as of March 2026:

- Stock price: ~$4.64 | Market cap: ~$206M

- Management NAV estimate (Sept 2025): $508M ($11.38/share basic, $9.21 fully diluted) — a ~59% discount on basic shares

- Cash + time deposits: $179M (year-end 2025) | Total debt: $0

- Fleet: 20 vessels (expanding to 26) | Vessels book value: ~$343M (Q3 2025)

- P/Tangible Book: ~0.33x | EV/EBITDA: ~0.38x

- FY2025 net income: $50M | Insider ownership (Vafias family): 30.1%

Read those numbers again. You can sell the ships for scrap, add the cash balance, and the sum exceeds the stock's market cap. The enterprise value is ~$27M for a fleet generating $50M in annual net income. At 0.33x tangible book, you're buying dollars for thirty-three cents.

Why does this opportunity exist? Governance risk and serial dilution. The Vafias family controls 30% of the stock, all management services flow through family entities, and the share count has more than doubled since a 2023 reverse split — including a recent $60M offering with warrants that could add another ~19M shares (~43% dilution from current levels). The market is pricing in continued dilution and related-party extraction. It's a legitimate concern.

What could re-rate it? The company initiated a new $10M buyback program in February 2026. If management follows through — buying back shares at 0.33x book instead of diluting — it would signal a shift in capital allocation philosophy. Meanwhile, the fleet is expanding to 26 vessels with zero debt, and tanker/drybulk rates remain supportive.

This is the tension in deep value: the assets are real, the discount is enormous, but the catalyst depends on management behavior that contradicts their track record. It requires more nuance, more monitoring, and a clear-eyed view of the risks. Not every deep value stock works out. But when the margin of safety is this wide, you don't need everything to go right — you just need the worst case not to happen.

The Filter in Practice

These three questions work as a sequential funnel, applied differently depending on the bucket:

Q1 — Valuation:

- GARP: Under 20x EBITDA, high ROIC, secular tailwinds

- Deep Value: Below tangible book, hard asset coverage, peer discount

Q2 — Why mispriced?

- GARP: Temporary drag masking quality (TDUP's Europe division)

- Deep Value: Cyclical trough, neglect, forced selling

Q3 — Catalyst:

- GARP: Earnings inflection, operational cleanup

- Deep Value: Activist pressure, commodity reversion, asset sales

Kill switch:

- GARP: Secular decline, no moat

- Deep Value: Solvency risk, secular decline, no asset floor

Most ideas die at Question 1 — the valuation either isn't compelling or the business is in secular decline. Of the survivors, maybe half have a legible mispricing reason. Of those, maybe half have a real catalyst. A list of 200 weekly ideas typically produces 3-5 names worth deep underwriting.

That's by design. In small cap investing, the edge isn't seeing more ideas — it's killing bad ones faster. The three-question filter is how I protect my scarcest resource: the time I spend on research that actually leads to conviction.

If you want to see this framework applied to real companies — with full financial analysis, variant perception scoring, and catalyst identification — that's what Pelican's research reports are built to deliver.

This is an investing framework for educational purposes only. Not investment advice. The author may hold positions in securities discussed. Always do your own due diligence before making investment decisions.

Get Daily Signals in Your Inbox

Join investors who start every morning with Pelican's top ideas.

Subscribe Free