Why I Built Pelican

I 8x'd my portfolio in 3 years investing in micro/small caps. Here's the exact process I use and how I turned it into a system that 450+ hedge funds use daily.

I built Pelican Alpha after deciding to codify what was working in my own investing. I've been investing in public equities since 2018, and over the last 3 years I've nearly 8x'd my money investing primarily in micro and small caps.

Pelican exists to solve the single biggest bottleneck I faced as an investor: turning over enough stones to find real opportunities, then underwriting them before alpha decay sets in. Below is my background, the exact process I follow, and how I turned it into a system.

My Background

I started my investing career at the multi-family office ICONIQ Capital, moved to the activist hedge fund Osmium Partners, and later managed a concentrated long-only strategy. Throughout my career, I've worked across activism, secular growth, long/short, and deep value strategies. My personal sweet spot — and where I've generated the most alpha — is in GARP (Growth at a Reasonable Price) and Special Situations.

I am a CFA charterholder with a background in economics and accounting from UCSB. I began my career in public accounting, which gave me the foundation I use today to analyze financial statements.

My strategies are inspired by Buffett, Munger, Greenblatt, Marks, Li Lu, Mohnish, Klarman.

Track Record

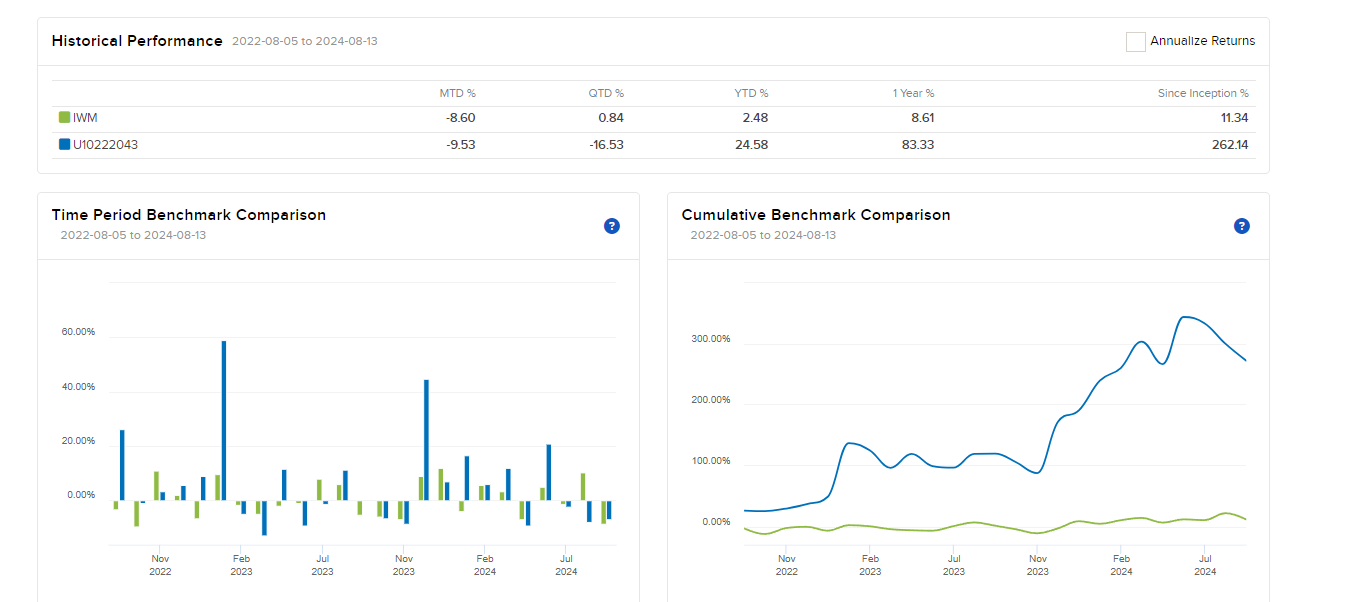

Over the last 3 years, since leaving my last job, I've nearly 8x'd my capital investing primarily in micro and small caps. My Roth IRA is up 124% over the last 12 months vs the S&P at 21%. A second account I manage is up 44% over the same period. The two years before that, I nearly 4x'd my capital.

I also run a public mock portfolio on Savvy Trader where every position, entry, and exit is fully transparent: savvytrader.com/ricardoleee93/pelican. The account is up 82% over the last year and 38% YTD (72% CAGR since inception in mid-2025). Follow it if you want to track my picks in real-time.

Some of my biggest winners in the small/micro space: ALTO, IMPP, TEN, IE, and GOOGL.

Past performance is not indicative of future results, and investing always involves risk.

How I Think About Markets

I don't believe markets are fully efficient. As Joel Greenblatt has pointed out, businesses don't fluctuate in value by 50% or 80% in a single year, yet their stock prices often do. If the market were a precise weighing machine, these swings wouldn't exist.

Small cap investing is largely a game of turning over stones. The inefficiency is real — most institutional investors can't own these names because of liquidity constraints, which means they're under-researched and mispriced far more often than large caps.

Everything I do is valuation-based. As Mauboussin said, everything should be a DCF. Unless a company has serious bankruptcy risk, there is almost always a price where that business becomes a bargain. The question is always: what is the business worth, and can I buy it for meaningfully less than that?

My mental model is simple:

- Look at a massive number of ideas (High Velocity).

- Kill the bad ones quickly (High Filter).

- Concentrate capital when you find the obvious winners (High Conviction).

The Process: 5 Steps

Step 1: Find Ideas Worth Investigating

You need a systematic process to surface ideas that are likely to be on the winning side of the trade BEFORE you even look at the fundamentals. Fish where the winners are.

What I screen for:

- Insider trading clusters — a CEO buying $5,000 is noise. A CEO, CFO, and chairman buying a combined $2,000,000 on the same day is a signal. Cluster buys are far more predictive than individual purchases. When the people who know the business best are putting their own money in, that's worth investigating.

- Congressional trades — love them or hate them, members of Congress trade on information advantages. These are public disclosures.

- 13F filings — what are the funds you admire actually buying? Osmium, Greenlight, Baupost, Pershing Square — their quarterly holdings tell you where smart money is allocating. If Klarman is buying something small and illiquid, that's a strong signal. (I wrote a detailed breakdown of how to read 13F filings if you want to go deeper on this.)

- Price target increases — when an analyst raises a target from $5 to $16, that's worth investigating, even if you don't trust sell-side targets blindly.

- Activist involvement — when an activist takes a 5%+ position and files a 13D, there's usually a catalyst coming. This is classic special situations investing.

- Material press releases — new contracts, management changes, strategic reviews, divestitures.

- Quantitative screens — businesses with 3-year revenue CAGR north of 10%, ROIC north of 10%, trading under 15x EBITDA.

Every day I screen thousands of data points across these 7 categories to find the most interesting signals. Each gets rated on a scale of 1-10 based on the strength of the signal.

Step 2: Gather Data and Understand the Business

Once you have names worth investigating, you need to do the actual work. This is the part most people skip or do superficially. You need to go through:

- Earnings call transcripts — what is management saying vs what the numbers actually show? Are they dodging questions? Are they sandbagging guidance? The transcript tells you things the 10-K never will.

- Annual reports and 10-Ks — business segments, risk factors, strategy, competitive positioning

- Proxy statements — how is management compensated? What are they incentivized to do? Do they own stock? Is their comp tied to revenue growth (potentially value-destructive) or ROIC (shareholder-aligned)? Munger said "show me the incentive and I'll show you the outcome" — the proxy is where you find the incentive.

- Financial statements — income statement, balance sheet, cash flow. Key ratios: ROIC, FCF margins, debt-to-equity, working capital trends

- Competitor data and industry reports — who are the peers, how does the target compare on margins, growth, valuation?

- Press releases and 8-K filings — material events, acquisitions, divestitures, management changes

- Institutional holdings and insider transactions — who's buying, who's selling, what's short interest?

- Web search — customer reviews, product sentiment, Glassdoor, industry news

For a single stock, you're looking at hundreds of pages of filings. This is where having a systematic process saves enormous amounts of time.

Step 3: Value the Business

What you do with this data depends on the type of business.

If a company is trading below tangible book, you want to know what the assets are actually worth — so you perform a liquidation value analysis. This is Graham-style net-net investing. If a company trades at 20x book, liquidation value is completely irrelevant.

For most businesses, a DCF is the anchor valuation. You're projecting free cash flows, applying a discount rate, and estimating a terminal value. The key is getting the assumptions right — and being honest about what you don't know.

Peer multiples — what are comparable companies trading at? If similar businesses trade at 12-15x EBITDA, is there a reason your target should trade at 8x? Maybe the discount is deserved. Maybe it isn't.

Historical multiples — what has this business traded at over the last 5 years? If it normally trades at 18x earnings and it's currently at 12x, is that a signal or a value trap?

Analyst price targets — I don't trust sell-side targets blindly, but the consensus gives you a market check.

You weight each method based on how relevant it is to the specific business, and you build a mosaic of what the business is worth. Not all methods deserve equal weight — and different business types call for different approaches.

Step 4: Adjust for Qualitative Factors

A raw valuation number isn't the final answer. You need to adjust for things the numbers alone can't tell you.

Management quality and alignment — does the management team own meaningful stock? Are their incentives aligned with shareholders? If they're compensated to grow revenue at all costs, they'll grow revenue at all costs — even if it destroys value. What's their track record at prior companies? (I wrote a detailed breakdown of how I grade management teams using an archetype-first framework.)

Moat durability — does the business have pricing power? Are customers locked in? Is there a network effect? Is the moat widening, stable, or narrowing? Are they gaining or losing market share?

Sentiment check — who owns the stock? What's short interest? What are insiders doing — buying or selling? What are institutions doing — accumulating or distributing? What does the sell side think?

These qualitative factors should move your valuation up or down. If peers trade at 20x EBITDA but your target has misaligned management, a shrinking moat, and heavy insider selling — maybe it deserves 15x. There's a deserved discount, and your job is to figure out how much.

Step 5: Make the Decision

After adjusting all your valuation methods, you arrive at a final implied value. Then, as Buffett said, if there's a sufficient margin of safety, you buy the stock.

If you make enough independent bets like this over time, you are likely to do well. The key words are "independent" and "over time." Concentrate when conviction is high, diversify across ideas, and be patient. As Li Lu has said, the ability to do nothing is one of the most valuable skills an investor can have.

How Pelican Systematizes This

I found that doing this process manually was taking me 20-30 hours per stock. So I built Pelican Alpha to automate the entire workflow and give retail investors institutional-level equity research.

1. Daily Signal Screening — Pelican screens 7 signal categories daily across thousands of data points (insider trades, congressional trades, 13Fs, price targets, activism, press releases, quant screens). Each signal is rated 1-10 based on strength. For example, a cluster buy from the CEO, CFO, and chairman totaling $2M scores much higher than a single director buying $5K.

2. Comprehensive Research — For the highest-rated signals, Pelican runs 35+ analysis prompts using all the raw data I mentioned above: transcripts, annual reports, proxies, financial statements, competitor data, industry reports, and web search. It ingests filings into a vector database and uses RAG to analyze them.

3. Scoring and Valuation — It scores the business's moat, scores the management team, scores sentiment. Then it performs valuation using DCF, peer comps, historical multiples, and price targets — many adjusted for the qualitative factors above. Then it calculates a weighted average to estimate fair value.

4. Context-Aware Analysis — Pelican doesn't evaluate all businesses the same way. A biotech should be analyzed differently than an energy cyclical. For SaaS, it looks at ARR, retention, and rule of 40. For banks, it's net interest margin and loan-to-deposit ratios. A company experiencing rapid growth like BROS should be evaluated differently than a late-stage mature company like SBUX. So Pelican classifies every business into one of 5 archetypes: Early-Stage Hypergrowth, Mature Compounder, Cyclical Operator, Asset-Based Operator, and Turnaround Candidate. The archetype changes the entire analytical framework.

5. AI Research Agent — Subscribers also get access to an AI agent with 31+ data tools that can pull live financials, search SEC filings, run structured analysis frameworks, and answer equity research questions in real-time.

450+ hedge funds currently receive our daily signals every morning via email, and that list is growing fast. I decided to open Pelican up to retail investors because I think individual investors deserve the same quality of research that institutions get. The whole point is to level the playing field.

A Personal Note

On a personal level, I was born in Brazil, I am ethnically Korean, and I moved to the U.S. at age 7. I'm currently living in Orange County with my parents and our dog, Xuxa.

When I'm not studying businesses, I'm usually playing basketball, watching MMA, or with my family.

I hope you enjoy the research.

Ricardo Lee

Founder, Pelican Alpha

Contact

Get Daily Signals in Your Inbox

Join investors who start every morning with Pelican's top ideas.

Subscribe Free